A Texas agency is about to issue the largest municipal bond deal in the history of the Lone Star State. The $3.5 billion deal will be a historic one, and it will help natural gas utilities that had billions of dollars in unexpected costs after a deadly winter storm two years ago.

On March 8 and 9, the Texas Natural Gas Securitization Finance Corp. plans to set a price for the taxable municipal bonds. They’ll be paid for by adding variable fees to the bills of the nine utilities’ customers.

There are things about the deal that could make some investors think twice. For one thing, it has a clause that says the bonds can be called if lawmakers decide to use the state’s extra money to pay off its debts early. Also, it is the biggest taxable municipal bond since at least 2020, according to data gathered by Bloomberg. For a volatile market to settle, this weight may need higher yields.

Said Jason Appleson, head of municipal bonds at PGIM Fixed Income-

“When you have a big deal like this, people pick their heads up — it will likely price with some healthy concessions”

“It’s not a small deal in any market but for taxable munis — it’s giant.”

Appleson says that another twist is that many of these securities, which are called rate-recovery bonds, are for electric companies and not natural gas utilities. That means investors will have to look at a different set of market risks and regulators. Customers could, for example, stop using natural gas and switch to electric stoves and heating.

More Latest news:

- Before The Fed Chair’s Testimony, Oil Goes Up For The Sixth Time In A Row

- Rivian Plans To Raise Money By Selling $1.3 Billion In Bonds, Shares Fall

After Winter Storm Uri hit much of the southern US in February 2021, this week’s sale is the end of a two-year process. Because it was cold in Texas for a long time, people needed more energy and utilities had to pay very high prices for natural gas, which they then passed on to their customers.

In that year, Texas lawmakers passed a law that made it possible for the costs to be securitized. This meant that utilities could spread the costs out over time, making it easier for bill-payers to pay. Since then, credit rating companies have looked at the deal, the underwriters have been chosen, and a state oversight board has given the deal the go-ahead.

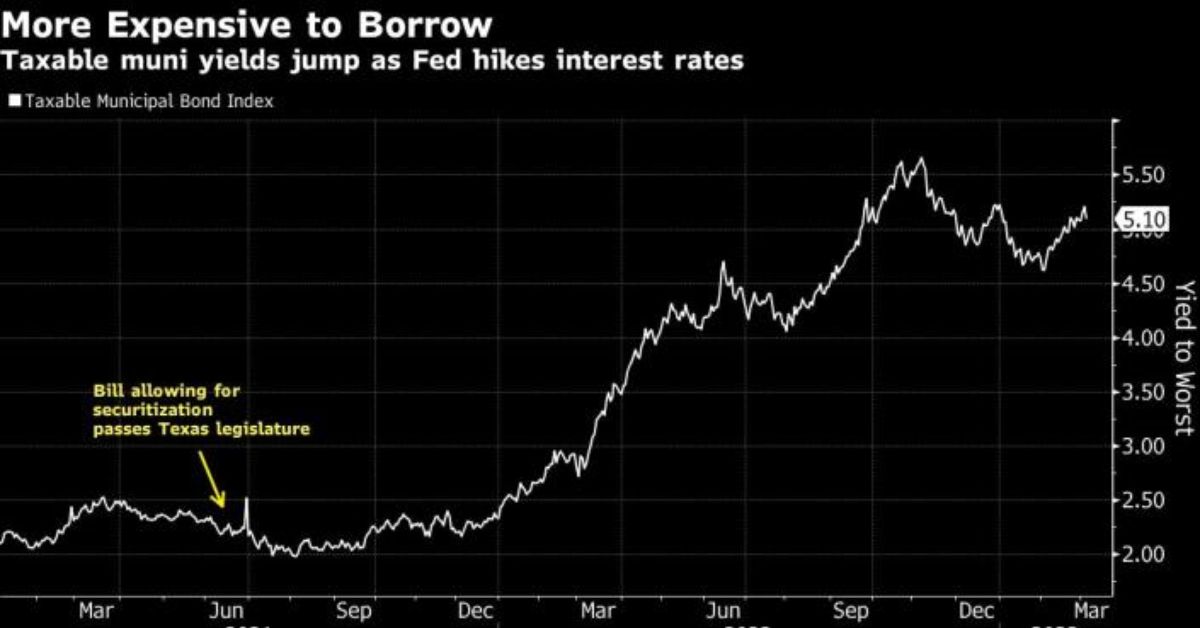

Since the deal was proposed, the whole macroeconomic picture has changed. For example, the Federal Reserve has been aggressively raising interest rates to slow down inflation. A benchmark index of taxable municipal bonds has a yield-to-worst of about 5.1%. This is about three percentage points higher than in June 2021, when Governor Greg Abbott signed House Bill 1520. As a result, the members of the board in charge of the sale raised the deal’s maximum interest rate from the 5% that the law required to 6.5%.

Early price talks for the two bonds in the offering, which have weighted average lives of six and 13.5 years, are around 125 basis points over Treasuries for the shorter segment and 162.5 for the longer segment, according to people with knowledge of the matter who asked not to be named because the talks are private.

Lead manager for the sale is Jefferies Financial Group Inc., and co-managers are Morgan Stanley and Hilltop Securities. There are also seven other firms in the group. Along the way, UBS Group AG and Citigroup Inc. had to drop out of the deal because of state laws that went into effect in 2021. The two bills stop the government from doing business with companies that Texas thinks have policies that hurt the gun and fossil fuel industries.

A spokesperson for Jefferies didn’t want to say anything, and a representative for the Texas Public Finance Authority, which is in charge of the sale, said that more information could be found in the bond documents. Moody’s Investors Service, Fitch Ratings, and Kroll Bond Rating Agency all gave the bonds their highest ratings.

The deal includes a limited make-whole call, which means that the issuer can buy back the bonds on any business day before April 1, 2026, or on any business day before that date. In the supplemental budget bill that Texas lawmakers introduced on March 2, they said that $3.9 billion from the general-revenue fund would be taken out to pay off the bonds. Bill-payers wouldn’t have to pay the extra money because of this change.

In a separate bill filed on Thursday, the winter storm was called a “public calamity,” giving the state agency the power to pay the bills if money is set aside. Some people who keep an eye on the market may be less likely to buy the bonds if they think they could be called. Emile Ernandez, a managing director at Kawa Capital in Florida, an asset management company that has invested in recovery bonds, says that recovery bonds are almost never callable.

“The fact that this bond can be called may make it harder for people to buy it,” said Scott Hofer, a senior research analyst at Income Research + Management for asset-backed securities. “Investors usually buy these bonds and keep them until they mature, but with this deal, especially the longer tranche, the duration uncertainty is very high.” “I hope this is the last recovery bond that has a call option with this much duration uncertainty,” he said.