As 2023 began, there were signs that inflation was finally being brought under control. This gave people hope that the Fed would try to control inflation in a less aggressive way and start cutting interest rates. Lotfi Karoui, the head of credit strategy at Goldman Sachs, says not to get too excited about that happening this year.

“No pivot. No cuts at all in 2023, “Karoui recently said that the Fed might think about lowering rates in the first or second quarter of 2024 at the earliest. Not everything is bad, though. Karoui thinks the U.S. economy will have a “soft landing” and that the chances of a recession are low.

There will always be opportunities for investors in the stock market, no matter what the future holds. Karoui’s analyst colleague at the banking giant, Kash Rangan, has been looking for stocks that he thinks are ready to move up from here. In fact, Rangan thinks that two stocks will rise by at least 70% over the next year. We put these choices into the TipRanks database to see what the rest of Wall Street thinks about them. Let’s see how things turned out.

Salesforce.com, Inc. (CRM)

One of the best-known names in tech and marketing is the first stock that has Goldman’s attention. Salesforce has been at the top of the Customer Relationship Management market for a long time. The company uses the popular SaaS model to offer software solutions and apps for sales, customer service, and marketing that run in the cloud. The company says that enterprise users won’t need IT experts to set up the software and that more than 150,000 customers have used Salesforce to improve their customer relations.

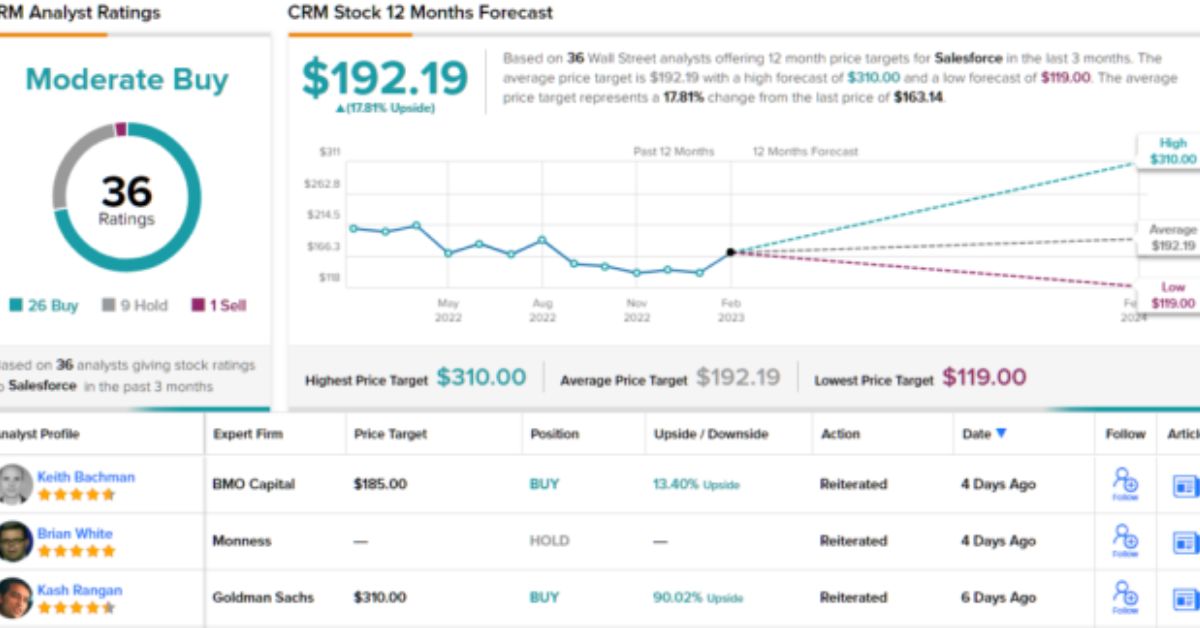

Over the past year, CRM’s share price has gone up and down, just like many other tech companies. Still, the company has been steadily making more money and bringing in more money. In the last reported quarter, fiscal 3Q23 (October quarter), sales went up 14% year over year to $7.84 billion, and non-GAAP EPS went up 10% year over year to $1.40. Salesforce has said that its revenue for fiscal Q4 will be between $7.93 billion and $8.03 billion. On March 1, we’ll find out if the company meets that goal.

In the meantime, Kash Rangan from Goldman has kept his firm’s Buy rating on this stock before the print. To explain his point of view, he writes, “We believe CRM is at an inflection point that can vault it into the upper echelons of highly valued tech companies. Looking towards the LT opportunity, where macro and restructuring hurdles ease, we expect top-line growth to re-accelerate and OM to exceed 30%…”

The analyst added-

“Adding to value-creating initiatives already underway (buybacks, workforce/real-estate reductions), Salesforce has a rare combination of market leadership (30% share) in the largest category within the $620bn software market (comprising 13% share and expected to have a 14-15% CAGR over next 3 years) and a largely untapped profitability lever within S&M”

Along with this picture, Rangan gives a price target of $310 per share for the next 12 months, which means a gain of 90% is coming. (Click here to see Rangan’s track record.) If there’s one thing that’s certain on Wall Street, it’s that analysts will pay more than their fair share of attention to big tech companies. This is definitely the case with Salesforce. Of the 36 recent analyst reviews on file, 26 say to buy, 9 say to hold, and only 1 says to sell, which adds up to a Moderate Buy rating.

GitLab Inc. (GTLB)

The second stock we’re looking at is GitLab, which is an innovative DevSecOps platform based on an open-source model that helps users do devops work faster and more efficiently while getting the most money back from the end product. GitLab’s open-source architecture makes it possible for users and collaborators to work together on planning, building, and deploying the platform. This is the main benefit of open-source architecture. Basic services are free, and upgrades can be bought through a subscription model.

GitLab was founded in 2014. Since then, the company has grown, and it now has more than 30 million registered users, 133 releases in a row, and more than 3,300 code contributors. Big companies like Nvidia, Siemens, T-Mobile, and even Goldman Sachs use the software.

GitLab released its financial results for the third quarter of its fiscal year 2023 in December. The top line grew by a huge 69% from the same time last year to an impressive $113 million. This was the most money the company made in a quarter since it went public in October 2021. The company usually has a net loss, and the Q3 non-GAAP EPS loss was 10 cents per share. This was the lowest quarterly net loss since the stock went public. Both the top and bottom lines of the report were much better than expected. GitLab will release its results for fiscal Q4 and the whole fiscal year 2023 on March 13.

Even though GitLab’s financial results look good, the recent slowdown in the tech industry has had an effect on the company. We’ve all heard that big companies like Google and Facebook have fired a lot of people, and after he took over Twitter, Elon Musk fired a lot of people there as well. GitLab is also cutting back on its staff. On February 9, the CEO of GitLab said that about 7% of its employees would be let go.

Kash Rangan, in his review of GTLB, continues to see this stock as a net-positive for investors, and writes of it: “We remind investors that GitLab has largely been able to sidestep significant pressures from the macro environment over the last two quarters. Given the broader trends we have seen emerge across software (absence of 4Q budget flush, layoffs), we would not be surprised if management re-evaluated their go-forward strategy in light of these dynamics.

While this may result in a reset to the +40% revenue growth figure outlined in early December, we remain constructive on the company’s ability to drive growth via the strong value proposition of its platform…”

More News:

- Citi Strategists Say That Investors Are Making More And More Short Bets On Stocks

- Due To Rising U.S. Rates, The Dollar Is Likely To Rise For The First Time Since September

Rangan added-

“Its growing partnerships with other cloud providers, namely Google Cloud, could also provide strong integrations with comparable AI functionality, which can improve its positioning across these point products”

Rangan has a “Buy” rating on GTLB shares because he thinks the risk-reward ratio is “positive.” His price target of $75 means that the stock could go up 70% in one year from where it is now. What do the other people on the Street think? It turns out that most other analysts think the same way. With 9 buys and 2 holds, the general opinion is that the stock is a Strong Buy.

Leave a Reply